Pay debt or invest first? That question sits at the center of a lot of money stress. You want progress, but each dollar only goes one place.

The good news is you do not need a one size fits all rule. The right move depends on a few numbers and a few life factors. Your debt rate matters. Your employer match matters. Your cash cushion matters too. So does your tolerance for market swings.

A smart plan often mixes both. You might grab free retirement match money, wipe out toxic debt, then shift hard into investing. Or you might attack high rate balances first because the return from paying them off beats what you are likely to earn in the market.

This guide breaks down the tradeoff in plain English. You will see when paying debt first tends to win, when investing first tends to make more sense, and how to choose the best next step for your situation right now.

At A Glance: The Core Tradeoff Between Debt Repayment And Investing

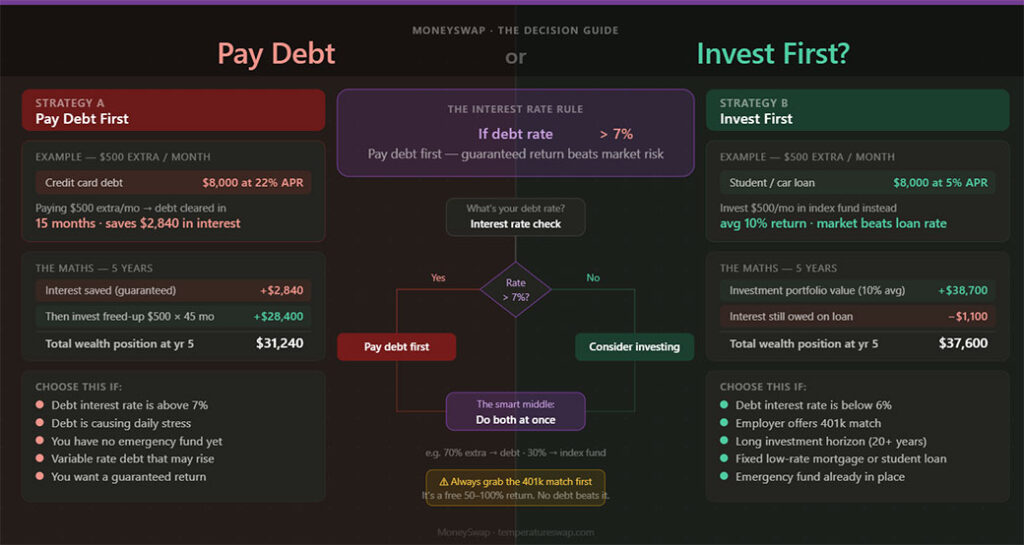

When you ask, “Pay debt or invest first?” you are comparing two uses for the same dollar.

If you pay debt, you get a guaranteed return equal to the interest rate on that debt. Pay off a credit card charging 22%, and you avoid 22% interest going forward. That is hard to beat.

If you invest, your return is uncertain. Stocks have produced strong long term returns, often around 10% annually before inflation over many decades, based on broad U.S. market history from sources like S&P Dow Jones Indices and Morningstar. Yet those returns do not show up on schedule. Some years are great. Some are painful.

So the core tradeoff is simple:

- Debt payoff gives you a known return

- Investing gives you a higher expected long term return in many cases, but with risk

- Liquidity changes the picture because extra debt payments are hard to pull back

- Employer retirement matches often beat both choices at the start

Here is the short version.

| If your dollar goes to | What you get |

|---|---|

| High interest debt payoff | Guaranteed savings at the debt rate |

| 401(k) with employer match | Immediate return from the match, often 50% to 100% on part of your contribution |

| Broad stock index investing | Long term growth potential, but no guarantee |

| Cash savings | Safety and flexibility, but lower return |

For most people, the best answer to pay debt or invest first is not all or nothing. It is a priority order.

The Criteria That Matter Most: Interest Rate, Employer Match, Risk, And Liquidity

Four factors should drive your choice.

Interest rate

Start here. The higher the rate, the stronger the case for debt payoff. A 24% card balance is a fire. A 3% fixed mortgage is not.

You can group debt roughly like this:

- 15% and up, usually pay this first

- 7% to 14%, gray area, depends on your goals and tax benefits

- 0% to 6%, investing often deserves more attention, especially over long periods

Employer match

If your job offers a 401(k) match, that often deserves top priority. Suppose your employer matches 100% of the first 4% of pay. If you contribute $4,000, your employer adds $4,000. That is an instant 100% gain before market growth.

If you skip that match to pay moderate rate debt, you may leave money on the table.

Risk

Debt payoff is predictable. Investing is not. If you need your money soon, market losses hurt more. If you have 20 years before retirement, short term drops matter less.

This is where behavior counts. If a 20% market drop would make you stop investing, paying debt first may fit you better. A plan only works if you stick with it.

Liquidity

Money sent to a lender stays there. Money held in savings stays available. That matters if your income is uneven or your emergency fund is thin.

Before you go hard on either debt payoff or investing, aim for a starter cash buffer. Many planners suggest at least $1,000 to $2,000 first, then a fuller emergency fund over time. The Consumer Financial Protection Bureau and Fidelity both stress emergency savings as a base for better financial decisions.

When Paying Debt First Usually Wins

Paying debt first usually wins when the debt is expensive, stressful, or risky to carry.

High interest debt

Credit cards are the clearest example. As of 2026, average credit card rates remain above 20% in many cases, according to Bankrate and Federal Reserve data trends. Few long term investors should choose stock investing over paying down a 20% balance.

If you are asking, “Pay debt or invest first?” and you have credit card debt at 22%, start there.

Variable rate debt

Variable APR debt adds uncertainty. Your rate can rise even if your payment does not drop the balance much. Paying this down reduces both cost and risk.

Thin cash flow

If debt payments make your monthly budget tight, debt payoff buys breathing room. Lower required payments reduce the odds of missed bills, overdrafts, or more borrowing.

Emotional and behavioral benefit

Math matters. Behavior matters too. Some people invest better once debt stress is gone. If debt keeps you up at night, wiping it out may improve your odds of staying consistent later.

Debt first often makes sense if you have:

- Credit card debt

- Payday loans

- Personal loans above market rates

- Buy now, pay later balances you are juggling poorly

- Any balance you are close to missing payments on

One exception stands out. If you have high interest debt and a strong employer match, you may split your money. Contribute enough to get the full match, then throw the rest at the debt. That hybrid approach works well for a lot of households.

When Investing First Usually Makes More Sense

Investing first usually makes more sense when your debt is cheap, your cash flow is stable, and time is on your side.

You get a strong employer match

This is the top case. Turning down a full match is often more costly than carrying low rate debt a bit longer. Even a 50% match on part of your contribution is hard to beat.

Your debt rate is low

A fixed student loan at 4% or a mortgage at 3.25% often does not need aggressive early payoff if you are behind on retirement savings. Over long periods, diversified stock investing has historically outperformed those rates, though no outcome is promised.

You need retirement compounding

Time matters more than many people expect. A 30 year old who invests $500 a month for 35 years will usually end up far ahead of someone who waits 10 years, even if the later investor puts in more per month. Compound growth rewards early action.

You want tax benefits

Retirement accounts offer tax advantages.

- Traditional 401(k) and IRA contributions may reduce taxable income

- Roth accounts offer tax free qualified withdrawals later

- Health Savings Accounts, if you qualify, offer triple tax advantages under current rules

Those benefits raise the value of investing.

Still, investing first does not mean ignoring debt. Keep paying at least the minimum on every loan. Protect your credit. Avoid fees. Keep a plan.

If you are deciding whether to pay debt or invest first and your only debt is a low fixed mortgage, investing often deserves the edge, especially if retirement savings are behind schedule.

Side-By-Side Comparison Of Common Financial Scenarios

Here is how the pay debt or invest first decision often plays out in real life.

| Scenario | Debt details | Investing option | Usually best move |

|---|---|---|---|

| Credit card balance at 24% | High cost, revolving | Taxable brokerage | Pay debt first |

| 401(k) match, card debt at 8% | Moderate debt | 100% match on first 4% | Get full match, then pay debt |

| Student loans at 5% | Fixed rate | Roth IRA | Split focus or invest first |

| Mortgage at 3.5% | Long term, low rate | 401(k) or IRA | Invest first in many cases |

| No emergency fund, loan at 6% | Some risk | Stock index fund | Build cash first, then split |

| Payday loan at 300% APR | Extreme cost | Any investment | Pay debt first, fast |

Scenario 1, high rate credit card debt

If you carry $8,000 at 22% APR, interest can eat up well over $1,500 a year if the balance stays high. Paying that off is like earning a guaranteed 22% return.

Scenario 2, employer match plus moderate debt

Suppose you have a car loan at 6% and your employer matches your retirement contribution dollar for dollar up to 4%. Grab the match first. After that, compare the car loan rate with your other goals.

Scenario 3, low rate student loans

If your student loans sit at 4% to 5% and you are in your 20s or 30s with decades to invest, regular retirement contributions often deserve priority.

Scenario 4, no cash reserves

This one gets missed. If you have no emergency fund, neither aggressive debt payoff nor investing should take every spare dollar. A surprise car repair can send you right back to credit cards.

Pros And Cons Of Each Approach

Each path has real upsides and tradeoffs.

Paying debt first

Pros:

- Guaranteed return equal to the interest rate

- Lower monthly obligations over time

- Less financial stress for many people

- Lower risk than investing in stocks

- Better cash flow once balances are gone

Cons:

- Missed market growth while you focus on payoff

- Lost employer match if you skip retirement contributions

- Less liquidity if all extra cash goes to debt

- Slower retirement progress if low rate debt takes too much attention

Investing first

Pros:

- More time for compound growth

- Access to employer match and tax breaks

- Better chance to build long term wealth

- Useful if your debt is low rate and fixed

Cons:

- Market losses are possible, especially in the short run

- Debt interest keeps accruing while you invest

- Harder to stay invested if debt stress feels heavy

- Some people underestimate the drag from high APR balances

A balanced approach

For many people, the best answer to pay debt or invest first is a split plan:

- Keep a starter emergency fund

- Contribute enough to get the full employer match

- Attack high interest debt

- Increase investing after toxic debt is gone

- Decide whether to prepay low rate debt based on your goals

This order works because it covers your biggest risks first. You protect cash flow. You take free money from your employer. Then you stop the worst interest from draining your budget.

Verdict: Which Priority Is Right For You Right Now?

If you want a simple rule for pay debt or invest first, use this one.

Pay high interest debt first. Take the full employer match first if one is offered. Invest first when your debt is low rate, fixed, and under control.

Ask yourself these five questions:

- Do you have any debt above 10% to 12%?

- Do you get a 401(k) match at work?

- Do you have at least a starter emergency fund?

- Are your minimum debt payments easy to cover each month?

- Are you behind on retirement savings for your age?

Your answers point to the next move.

- If you have high APR debt, focus there

- If you have a match, contribute enough to get all of it

- If you have no emergency fund, build one before going all in

- If your debt is low rate and stable, push more toward investing

Personal finance is not a purity contest. You do not win by picking one side forever. You win by putting each dollar where it does the most good right now.

That is the real answer to pay debt or invest first. Choose based on rate, match, risk, and liquidity. Then review the plan every few months as your balances, income, and goals change.

Frequently Asked Questions about Paying Debt or Investing First

What factors should I consider when deciding whether to pay debt or invest first?

Consider your debt interest rate, employer retirement match, your cash emergency fund, risk tolerance, and liquidity needs. High-interest debt often calls for repayment first, while low-rate debt and strong employer matches can favor investing early.

Why is an employer 401(k) match important in deciding to invest first?

Employer matches provide an immediate, guaranteed return—often 50% to 100% on contributions—making it financially smart to contribute enough to earn the full match before focusing on paying down moderate debt.

When does paying off debt usually make more sense than investing?

Paying off debt first is usually best if you have high-interest debt like credit cards, variable rate loans, or if debt payments strain your cash flow. It offers a guaranteed return equal to the debt interest rate and reduces financial stress.

Is it better to invest first if I only have low-rate debt like a mortgage or student loan?

Often yes. When your debt is low-rate and fixed, investing can yield higher long-term returns, especially if you benefit from employer matches or tax-advantaged accounts. Maintaining at least minimum debt payments is still essential.

How much cash should I keep before aggressively paying debt or investing?

Experts recommend starting with a cash cushion of $1,000 to $2,000 as a starter emergency fund. This liquidity protects you from unexpected expenses and helps avoid additional debt while pursuing debt payoff or investing.

Can I split my money between debt repayment and investing?

Yes, a balanced approach often works best. For example, contribute enough to capture your full employer match, then apply extra funds to high-interest debt. After eliminating toxic debt, increase investing contributions to build wealth.

{kind=link}