Student loan payoff strategies work best when you stop guessing and start with the numbers. If your balance feels scattered across different servicers, rates, and repayment plans, you’re dealing with a planning problem before a money problem. The fix starts with clarity.

Your goal is not to throw random extra payments at your loans and hope for the best. Your goal is to pick a plan that fits your cash flow, lowers interest when possible, and stays realistic through job changes, rent increases, and plain old fatigue.

A smart payoff plan usually comes down to four moves. Know what you owe. Choose a repayment method that matches your budget and motivation. Cut borrowing costs where you can. Then build a system you’ll keep following month after month. Do those well, and your student loan payoff strategies stop being ideas and start becoming progress.

Start By Understanding Exactly What You Owe

Before you pick between aggressive payoff and lower monthly payments, gather the full picture. Many borrowers have a mix of federal direct loans, older FFEL loans, Perkins loans, or private student loans. Each type follows different rules for interest, repayment, deferment, forgiveness, and refinancing.

Start with four facts for every loan:

- Current balance

- Interest rate

- Loan type, federal or private

- Minimum monthly payment

If you have federal loans, check your details through your loan servicer and your Federal Student Aid account. For private loans, log in to each lender portal and download the latest statements. Put everything into one simple tracker, even a notes app or spreadsheet works.

Then calculate your weighted average interest rate and identify your most expensive debt. A private loan at 10 percent deserves a different strategy than a federal loan at 3.5 percent with flexible payment protections.

Next, check the repayment status of each loan. Are you on the standard plan, graduated repayment, an income-driven repayment plan, or a temporary forbearance? This matters because some plans lower your payment but increase total interest over time.

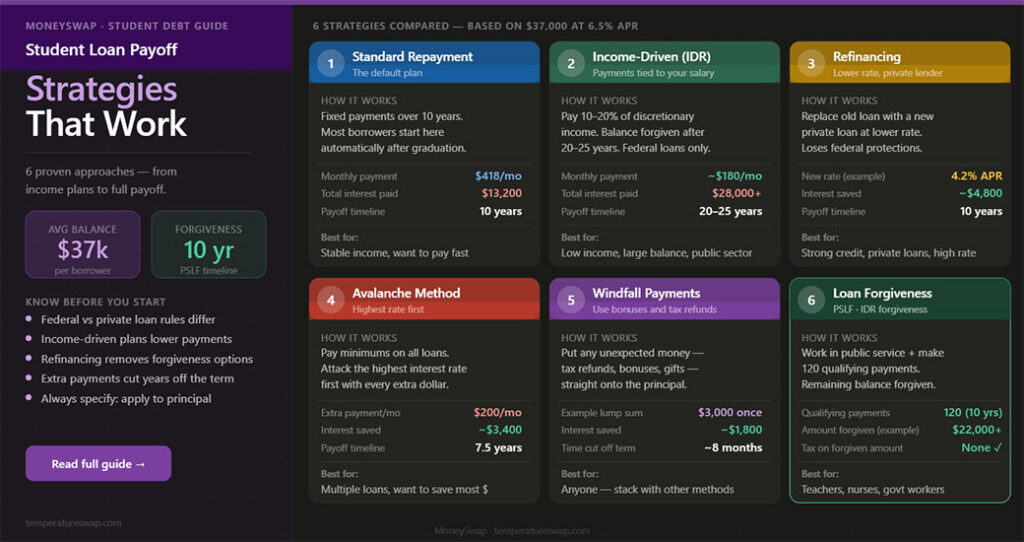

Also review whether any federal loans qualify for Public Service Loan Forgiveness, teacher loan forgiveness, or state-based repayment help. If forgiveness is on the table, your best student loan payoff strategy might not be early payoff at all. In that case, paying the least required while meeting program rules often makes more sense.

One more step. Look at your monthly budget beside your loan list. If your rent, food, insurance, and emergency savings already strain your income, an ultra-aggressive payoff target may fail by month three. Good plans are exact. Great plans are exact and survivable.

Choose The Best Repayment Strategy For Your Budget And Goals

Once you know your loan details, match them to your goal. Most borrowers fit into one of three buckets.

First, you want the lowest total interest cost. In that case, you’ll focus extra payments on the highest-rate loan while making minimum payments on the rest.

Second, you want psychological momentum. Then you may prefer knocking out the smallest balance first so you see quick wins.

Third, you need payment flexibility because your income is uneven or tight. Then lowering required payments first may be smarter than pushing extra money every month.

Your best choice depends on your timeline, income stability, and federal loan protections. For example, if you work in government or at a qualifying nonprofit and expect Public Service Loan Forgiveness, paying extra on eligible federal loans often works against your goal. If your loans are private and carry high rates, fast payoff often saves serious money.

Set a target date. A five-year payoff plan and a ten-year payoff plan create different monthly demands. Then decide how much extra you can send each month after minimum payments, emergency savings, and any retirement match from your employer.

Automation helps here. Schedule the minimum payment on every loan. Then set one separate automatic extra payment toward your target loan a day or two after payday. This keeps your student loan payoff strategies consistent instead of depending on willpower.

If your cash flow changes, review the plan. A strategy is not a contract. It is a tool.

Avalanche Vs Snowball: Which Payoff Method Fits You Best

The avalanche method means you pay minimums on all loans and direct extra money to the highest interest rate first. Once that loan is gone, you roll its payment into the next highest rate. This method usually saves the most money.

The snowball method means you pay minimums on all loans and attack the smallest balance first. When that balance is gone, you roll the freed-up payment into the next smallest loan. This method builds motivation faster because you get early wins.

Here is the practical difference. Suppose you have three loans:

- $3,000 at 5 percent

- $8,000 at 8 percent

- $20,000 at 6 percent

With avalanche, the 8 percent loan gets your extra money first. With snowball, the $3,000 balance goes first. Avalanche often wins on math. Snowball often wins on behavior.

So which should you choose?

Pick avalanche if:

- You care most about lowering total interest

- You stay motivated by spreadsheets and long-term savings

- Your highest-rate loans are private and expensive

Pick snowball if:

- You need quick progress to stay consistent

- You feel stressed by having many open balances

- Small wins keep you from giving up

A hybrid approach also works. You might clear one tiny loan for momentum, then switch to avalanche. The best student loan payoff strategies are the ones you keep following.

Lower Your Costs Before You Pay Extra

Paying extra helps, but cutting your interest cost first often helps more. This is where many borrowers leave money on the table.

Start with the simple wins. Ask whether your lender or servicer gives an autopay discount. Many federal loan servicers and private lenders reduce your rate by 0.25 percentage points when you enroll. That sounds small. Over years, the savings add up.

Next, check whether your lender offers a rate reduction for strong payment history or loyalty, especially if you also bank there. Not every lender does. Some do.

Then review your budget for money leaks you can redirect every month. A smaller recurring cut beats one heroic payment. If you free up $75 from subscriptions, delivery spending, or a cheaper phone plan, that becomes a repeatable extra payment. Over a year, that is $900 before interest savings.

You should also think carefully about where extra dollars go. If you have a federal loan at a low fixed rate and a private loan at a high variable rate, the private loan usually deserves priority. Risk matters as much as rate.

Tax benefits matter too, though not for everyone. The student loan interest deduction can reduce taxable income for eligible borrowers, subject to IRS limits and income phaseouts. It will not erase your debt, but it affects your true borrowing cost.

Another key step is avoiding unnecessary pauses. Forbearance and deferment can help during hardship, yet unpaid interest often keeps growing, especially on many loan types. A short-term break fixes cash flow today but can make payoff slower and more expensive later. Use those tools when needed, not by default.

When To Refinance, Consolidate, Or Enroll In Income-Driven Repayment

These three options sound similar. They are not.

Refinancing means replacing one or more existing loans with a new private loan, ideally at a lower interest rate. This option makes the most sense when you have solid credit, stable income, and little need for federal protections. If you refinance federal loans into a private loan, you give up federal benefits such as income-driven repayment plans, generous hardship options, and access to federal forgiveness programs. For some borrowers, the lower rate is worth it. For others, that trade is too costly.

Consolidation usually refers to a federal Direct Consolidation Loan. This combines eligible federal loans into one new federal loan. Consolidation simplifies billing and may help you qualify for certain repayment plans or forgiveness paths. Still, it does not usually lower your interest rate. Your new rate is the weighted average of your existing federal rates, rounded up slightly.

Income-driven repayment, or IDR, sets your federal student loan payment based on income and family size. For borrowers with low or uneven income, IDR creates breathing room and reduces the chance of delinquency. Some plans also offer forgiveness after a set repayment period if a balance remains. The tradeoff is slower payoff and, at times, more total interest.

Use a simple filter:

- Refinance if your rate is high, your income is stable, and you do not need federal safety nets.

- Consolidate if you need one federal payment or need access to a federal plan.

- Choose IDR if your payment is too high under the standard plan or if you are pursuing forgiveness.

Good student loan payoff strategies reduce cost first, then speed up payoff.

Build A Payoff Plan You Can Stick With Month After Month

The best plan on paper fails if your system is weak. You need a setup that survives busy months, surprise bills, and dips in motivation.

Start by choosing one monthly extra payment amount. Make it exact. Not “whatever is left.” Pick a number such as $100, $250, or 5 percent of your take-home pay. If your income changes from month to month, set a floor and a stretch amount. For example, your floor is $50 extra. Your stretch target is $200 when income is higher.

Next, create a repayment order. Write down which loan gets extra money first and why. If you use avalanche, list loans from highest rate to lowest. If you use snowball, list them from smallest balance to largest. This removes decision fatigue.

Then automate as much as possible:

- Minimum payments on all loans

- One extra payment to your target loan

- A monthly transfer to emergency savings

That third step matters. Without a cash buffer, one car repair can force you into new debt or missed payments. Even a starter emergency fund of $500 to $1,000 gives your payoff plan some stability.

Track progress in a way you will keep using. A spreadsheet is fine. So is a note on your phone. Update balances once a month, not every day. Daily checking tends to drain motivation because loan balances move slowly.

You also need rules for windfalls. Decide now where tax refunds, bonuses, side gig income, or cash gifts will go. A simple split works well:

- 50 percent to your target loan

- 30 percent to emergency savings or high-interest credit card debt

- 20 percent for planned spending

This keeps your life moving while debt keeps shrinking.

Review your plan every three to six months. If your income rises, increase extra payments. If your housing cost jumps, lower the extra amount without guilt and keep the habit alive. Consistency beats intensity.

One more point. If you are paying off student loans while carrying credit card debt above roughly 20 percent, the credit card balance often deserves top priority. Mathematically, that debt usually costs more. Student loan payoff strategies work best when they fit your full financial picture, not one balance in isolation.

Conclusion

Student loan payoff strategies start with one simple move. Get clear on every balance, rate, and repayment option you have. From there, choose a method that fits how you think and how you budget. Cut costs before sending extra money. Then automate a plan you can keep going.

You do not need a perfect setup on day one. You need a workable one. If your strategy matches your income, protects your cash flow, and points extra money at the right loans, progress will show up. And once it does, staying with the plan gets a lot easier.

Student Loan Payoff Strategies: Frequently Asked Questions

What is the first step in creating an effective student loan payoff strategy?

The first step is to gather clear details about each loan, including current balance, interest rate, loan type, and minimum monthly payment. This clarity helps you understand your total debt and plan payments realistically.

How do the avalanche and snowball methods differ in paying off student loans?

The avalanche method targets loans with the highest interest rates first to save money over time, while the snowball method pays off the smallest balances first to build motivation quickly. Both have benefits depending on your goals and mindset.

When should I consider refinancing my student loans?

Refinancing makes sense if you have a high-interest rate, stable income, and don’t need federal protections like income-driven repayment or loan forgiveness, because refinancing federal loans into private loans means losing those federal benefits.

Can income-driven repayment plans help with managing student loan payments?

Yes, income-driven repayment adjusts your federal loan payments based on income and family size, offering flexibility during tight financial periods. It may also lead to loan forgiveness after a set time but can increase total interest over the long term.

What strategies can lower my student loan costs before making extra payments?

You can lower costs by enrolling in autopay discounts, negotiating rate reductions with lenders, cutting budget leaks to free up funds, and avoiding unnecessary deferment or forbearance which can increase unpaid interest.

How important is automating payments in student loan payoff strategies?

Automation is crucial as it ensures consistent minimum payments and scheduled extra payments, reducing reliance on willpower. It also helps maintain progress even through busy months, income changes, or unexpected expenses.

{kind=link}