How to pay off $20k in debt starts with a clear plan, not panic. A $20,000 balance feels heavy when interest keeps adding up and every paycheck already has a job. Still, you do not need a perfect income or a lucky break to make steady progress.

You need numbers, a method, and a few smart changes you can keep up. This guide shows you how to pay off $20k in debt step by step. You will list each balance, build a lean budget, pick a payoff method, cut interest, raise extra cash, and stay on track when motivation dips. If you stick with the plan, your debt stops feeling like one giant problem and turns into a series of smaller moves you can handle.

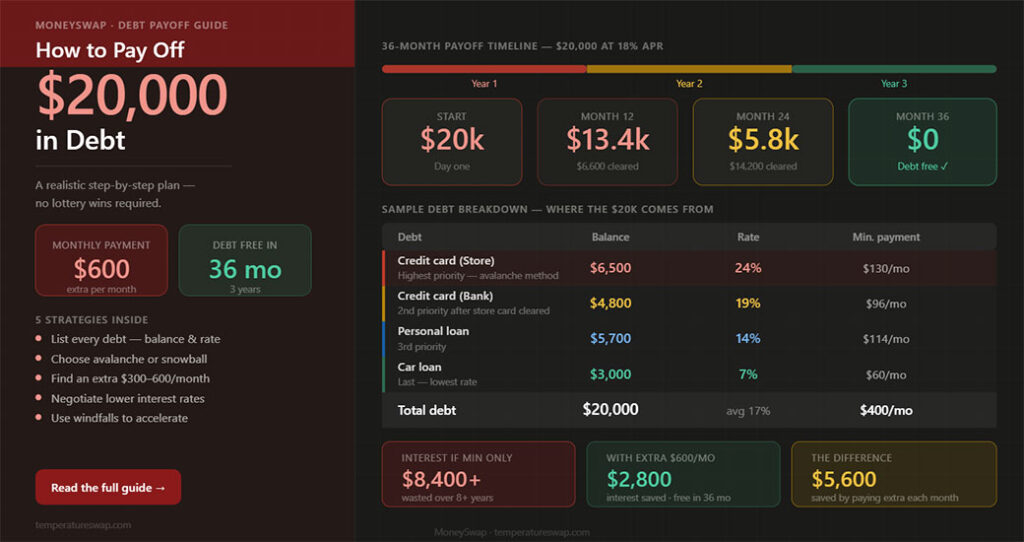

Figure Out Exactly What You Owe And What It’s Costing You

If you want to know how to pay off $20k in debt, start with a full debt list. Guessing keeps you stuck. Exact numbers help you see where your money goes and which balances hurt you most.

Write down each debt in one place. Use a spreadsheet, notes app, or paper. Include:

- Creditor name

- Total balance

- Interest rate

- Minimum payment

- Due date

- Type of debt, such as credit card, personal loan, auto loan, or medical bill

Next, calculate how much interest each balance adds every month. A credit card with a $7,000 balance at 27 percent APR costs far more than a $7,000 loan at 9 percent. That difference matters.

Here is a simple example:

- Card A, $8,000 at 26 percent, minimum $240

- Card B, $5,500 at 19 percent, minimum $165

- Personal loan, $4,500 at 11 percent, minimum $145

- Medical bill, $2,000 at 0 percent, minimum $50

That total equals $20,000, but the pain is not spread evenly. Card A drains the most money through interest. So, your plan should reflect that.

Also, check for late fees, annual fees, and penalty APRs. If you missed payments, your rate might have jumped. Review the last two statements for each account.

At this stage, total your minimum payments. Then total your after tax monthly income. Those two numbers show your starting gap. Once you know the size of the problem, you can build a plan around facts instead of stress.

Build A Bare-Bones Budget That Frees Up Extra Cash Every Month

A debt payoff plan fails fast if your budget is vague. You need a bare-bones budget, one built to cover needs first and send every extra dollar to debt.

Start with your monthly take-home pay. Then list your fixed costs:

- Rent or mortgage

- Utilities

- Insurance

- Minimum debt payments

- Groceries

- Gas or transit

- Child care

- Phone

After that, review the last 60 to 90 days of spending. Bank statements tell the truth. Sort every purchase into one of three buckets:

- Need

- Nice to have

- Easy cut

Easy cuts often include takeout, delivery fees, extra subscriptions, impulse shopping, rideshares, and convenience spending at gas stations or big box stores.

Your goal is not to make life miserable. Your goal is to free up cash for a defined period. Even an extra $300 to $700 per month changes your payoff timeline.

Try this quick budget reset:

- Pause subscriptions you barely use

- Set a weekly grocery cap

- Plan low-cost meals

- Cut shopping apps from your phone

- Move dining out to one set amount each month

- Lower entertainment spending for 90 days

Suppose you free up:

- $120 from eating out less

- $80 from subscriptions and memberships

- $150 from lower grocery waste

- $100 from shopping cuts

That gives you $450 more each month. Over a year, that is $5,400 sent to debt, before any side income or interest savings.

Keep the budget simple. If you make 20 categories, you will stop using it. Focus on the few changes with the biggest payoff.

Choose A Debt Payoff Method You Can Stick With

Once your budget frees up extra money, choose how to pay down the balances. The best debt payoff method is the one you will follow for months, not the one that sounds best for one day.

The two main methods are debt avalanche and debt snowball.

Debt avalanche means you:

- Pay minimums on all debts

- Put every extra dollar toward the highest interest rate first

- Move to the next highest rate after the first balance is gone

This method saves the most money on interest. If your rates are high, the savings add up fast.

Debt snowball means you:

- Pay minimums on all debts

- Put every extra dollar toward the smallest balance first

- Roll that payment into the next smallest debt after you clear the first one

This method gives faster wins. For some people, those early wins matter more than pure math.

Here is the simple choice:

- Pick avalanche if you care most about total cost

- Pick snowball if you need quick momentum

There is also a hybrid option. You might knock out one small balance first for a mental win, then switch to highest interest after that.

If you are serious about how to pay off $20k in debt, automate the plan. Set automatic minimum payments on every debt. Then schedule one extra payment each payday to your target debt. Automation cuts missed payments and keeps you moving.

Do not split extra money across every account. That feels productive, but usually slows progress. Focus works better. One target at a time gives you a visible finish line and a stronger sense of progress.

Lower Your Interest Rates And Negotiate Your Bills

Paying off debt gets easier when less of your payment goes to interest and fees. A few phone calls can save hundreds, sometimes more.

Start with your credit card issuers. Ask for a lower APR. Be direct. You can say, “I have been making payments and I want to keep this account in good standing. What rate reduction options do you have?” If your credit improved or you have a solid payment record, your odds rise.

Next, review these options:

- Balance transfer card with a 0 percent intro APR

- Debt consolidation loan with a lower fixed rate

- Hardship program through your card issuer

- Nonprofit credit counseling agency debt management plan

A balance transfer works best if you qualify for a low fee and can pay the balance before the promo period ends. A consolidation loan helps when the new rate is lower and the payment fits your budget.

Also, negotiate regular bills. Lower bills create more room for debt payments. Call and ask about:

- Internet discounts

- Cell plan changes

- Insurance rate reviews

- Medical bill reductions or payment plans

- Utility budget plans

For example, cutting $40 from your phone bill, $35 from internet, and $60 from insurance frees up $135 each month. That is $1,620 per year for debt payoff.

Be careful with debt settlement firms that ask for large upfront fees or tell you to stop paying creditors. Those plans carry risk, including credit damage and possible tax issues on forgiven debt.

If high interest is the main reason you feel stuck, this step matters a lot. Lower rates shorten your timeline even if your income stays the same.

Increase Your Monthly Debt Payments With New Income Streams

Budget cuts help, though income growth speeds up debt payoff more than most people expect. Even a modest side income can turn a five year plan into a much shorter one.

Focus on income sources you can start fast. Good options include:

- Overtime at your current job

- Freelance work based on skills you already have

- Food delivery or grocery delivery

- Pet sitting or dog walking

- Babysitting

- Weekend retail or event work

- Selling unused items

- Tutoring

- House cleaning or yard work

Pick one or two options with the best mix of speed, pay, and fit for your schedule. Then send that money straight to debt. Do not blend it into regular spending.

Here is what extra income looks like over time:

- $200 per month equals $2,400 per year

- $500 per month equals $6,000 per year

- $800 per month equals $9,600 per year

Add that to the budget cuts from earlier and your payoff pace changes fast. If you free up $450 from your budget and earn $500 more each month, you now have $950 extra for debt. That is $11,400 per year, on top of your minimum payments.

Use a separate checking account or savings bucket for side income if needed. Once the balance builds, make one extra debt payment each week or each payday.

If you get windfalls, use them with intention:

- Tax refund

- Bonus

- Cash gifts

- Refund checks

- Sale proceeds from items you no longer need

You do not need a second career to learn how to pay off $20k in debt. You need a temporary income plan with a clear purpose.

Avoid Common Setbacks And Stay Motivated Until The Balance Hits Zero

Debt payoff rarely moves in a straight line. A car repair, school expense, or slow work month can throw you off. The goal is to avoid turning one setback into a full stop.

Start with a small emergency buffer. Even $500 to $1,000 helps you handle basic surprises without adding new debt. Build that first if you have nothing set aside.

Next, watch for common mistakes:

- Keeping credit cards active for random spending

- Failing to track progress each month

- Paying extra one month, then giving up after a setback

- Ignoring due dates and getting hit with fees

- Rewarding progress with new debt

You also need visible progress. Motivation fades when the plan lives only in your head. Create a simple tracker with:

- Starting balance

- Current balance

- Amount paid this month

- Total interest rate changes you secured

- Debt free date estimate

Review your numbers once a week. Not daily. Daily checking often raises stress without helping.

Try a few practical ways to stay engaged:

- Mark each paid off debt on paper

- Share your goal with one trusted person

- Set mini targets for each $1,000 paid off

- Keep one written reason for getting debt free, such as lower stress or more room in your budget

If you slip, reset fast. Missed a week. Fine. Make the next payment. Overspent one weekend. Cut back the next. Consistency matters more than perfection.

This part of how to pay off $20k in debt is mental as much as financial. A plan works when you keep showing up for it.

Create A Simple Next-Step Plan For The First 90 Days

The first 90 days shape the whole debt payoff plan. Keep this phase simple and exact. You are building habits, lowering costs, and creating early proof that your plan works.

Use this timeline.

Days 1 to 7

- List every debt, rate, minimum, and due date

- Add up total minimum payments

- Review the last 60 to 90 days of spending

- Choose your debt payoff method

- Set up automatic minimum payments

From Days 8 to 30

- Build your bare-bones budget

- Cut or pause nonessential spending

- Call credit card companies to ask for lower rates

- Ask about hardship options if needed

- Sell a few unused items for a quick cash start

Days 31 to 60

- Start one side income source

- Send all extra money to one target debt

- Track progress weekly

- Build a small emergency buffer if you do not have one

- Adjust your budget based on what happened in month one

Days 61 to 90

- Review total debt paid down

- Check whether your chosen method still fits

- Renegotiate any bills you skipped earlier

- Increase side income hours if your schedule allows

- Set a six month target in dollars, not vague hopes

A sample 90 day goal might look like this:

- Cut spending by $400 per month

- Earn $300 extra per month

- Lower monthly bills by $100

- Put a total of $800 extra per month toward debt

That equals $2,400 in extra payments over 90 days, before minimums.

If you want a practical answer for how to pay off $20k in debt, this is it. Know your numbers. Cut costs. Raise income. Focus your payments. Repeat the process each month until the balance reaches zero.

Frequently Asked Questions About Paying Off $20k in Debt

What is the first step in paying off $20,000 in debt?

Begin by listing every debt with its balance, interest rate, minimum payment, and due date. Knowing exact numbers helps you understand your true financial situation and identify which debts are costing you the most in interest.

How can I create a budget that helps pay off debt faster?

Build a bare-bones budget prioritizing essential expenses and minimum debt payments. Cut or pause nonessential spending like subscriptions, dining out, and impulse shopping to free up extra cash to put toward debt each month.

Which debt payoff method should I choose to pay off $20k in debt?

Choose the debt avalanche method if you want to save money on interest by paying off high-interest debts first, or the debt snowball method if you prefer quick wins by paying off smaller balances first. Pick the method you can stick with consistently.

Can negotiating interest rates help me pay off $20k in debt faster?

Yes, calling creditors to request lower APRs or exploring balance transfers and consolidation loans can reduce interest costs, letting more of your payment go toward the principal and speeding up debt payoff.

What are some quick ways to increase income to pay off $20k debt faster?

Consider side jobs like freelance work, delivery services, pet sitting, selling unused items, or part-time retail work. Even modest additional income can significantly accelerate your debt payoff timeline.

How can I stay motivated when paying off a large debt like $20,000?

Track your progress visually, set small milestones, share your goals with someone you trust, and keep a clear reason for becoming debt-free. Prepare for setbacks and focus on consistency over perfection to maintain momentum.

{kind=link}