Avalanche vs snowball method is one of the first choices you face when you want to pay off debt faster. Both plans are simple. Both work. Yet they push you in different ways.

The avalanche method saves more money by targeting the highest interest rate first. The snowball method builds momentum by knocking out the smallest balance first. Your best pick depends on your debt mix, your habits, and how you stay motivated when progress feels slow.

This review compares avalanche vs snowball method in plain language. You’ll see how each one works, where each method shines, where each one falls short, and how they stack up against other debt payoff approaches. By the end, you should know which plan gives you the best shot of sticking with it and getting out of debt.

At A Glance

When people compare avalanche vs snowball method, they’re usually asking two questions.

- Which one saves more money?

- Which one helps you stay consistent?

Here’s the short answer.

| Method | First debt you attack | Main benefit | Main tradeoff | Best for |

|---|---|---|---|---|

| Avalanche method | Highest APR debt | Lowest total interest cost | Early wins may take longer | You care most about math and cost |

| Snowball method | Smallest balance | Fast psychological wins | You often pay more interest overall | You need momentum and visible progress |

With both methods, you make minimum payments on all debts and put any extra money toward one target debt. Once you clear that debt, you roll its payment into the next one.

That shared structure matters. The real difference in avalanche vs snowball method is the order of attack.

A quick example helps.

Say you owe:

- Credit card A, $1,000 at 29% APR

- Credit card B, $4,000 at 18% APR

- Personal loan, $7,000 at 10% APR

Under avalanche, you hit Credit card A first because it has the highest APR. Under snowball, you also hit Credit card A first because it’s the smallest balance. But if the smallest balance had a lower APR than another debt, the two methods would split.

So the comparison is not about right versus wrong. It’s about efficiency versus behavior. Your numbers matter. Your habits matter too.

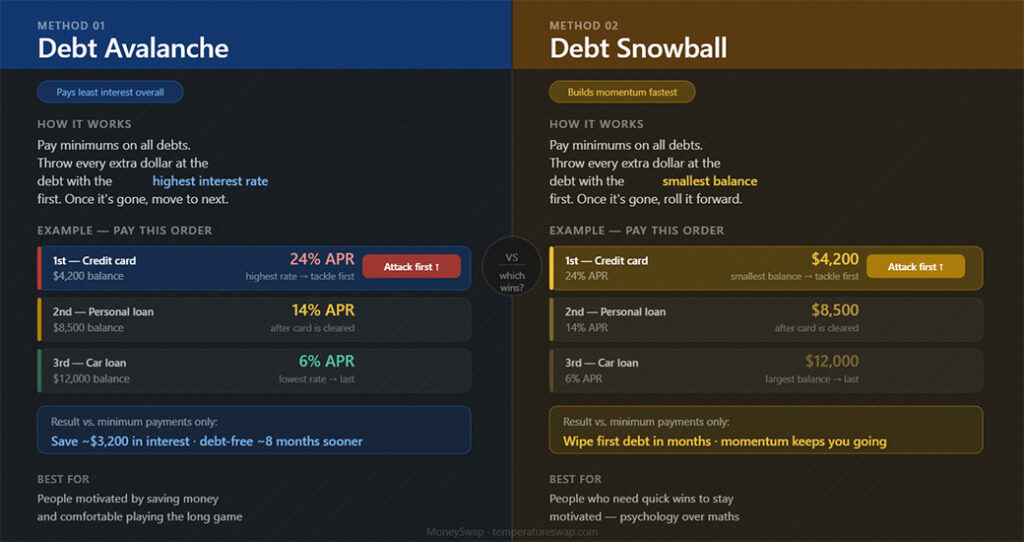

How The Avalanche And Snowball Methods Work

The avalanche vs snowball method debate starts with debt ranking.

Avalanche method

You list all debts by interest rate, from highest APR to lowest APR. Then you:

- Pay the minimum on every debt

- Put every extra dollar toward the highest APR debt

- Move to the next highest APR after the first one is gone

This method cuts interest charges faster. Credit card debt usually sits at the top because rates are often far above auto loans, federal student loans, or mortgages.

Example order:

- Store card at 31% APR

- Credit card at 24% APR

- Personal loan at 12% APR

- Car loan at 6% APR

You attack the store card first, even if the balance is not the smallest.

Snowball method

You list debts by balance, from smallest to largest. Then you:

- Pay the minimum on every debt

- Put every extra dollar toward the smallest balance

- Roll that payment into the next smallest debt after payoff

This method creates quick wins. If your first balance is small, you may clear one account in a month or two. For many people, that visible progress matters more than interest savings on paper.

What stays the same

In avalanche vs snowball method, a few rules do not change.

- You need a fixed monthly extra payment amount

- You must avoid adding new debt while paying down old debt

- You need an emergency buffer, even a small one, so one surprise bill does not knock you off track

Without those basics, either plan breaks down. The method helps. Your follow through decides the result.

Evaluation Criteria

To judge avalanche vs snowball method fairly, you need more than one yardstick. A method is not good only because the math looks better. A method is not good only because you feel better in week one either.

Here are the criteria that matter most.

1. Total interest paid

This is the biggest advantage of avalanche. By clearing the highest APR first, you reduce the most expensive debt sooner. According to consumer finance guidance from the Consumer Financial Protection Bureau, interest costs can keep balances growing when payments stay low. A high rate debt should get attention fast.

2. Time to first win

Snowball often wins here. If your smallest balance is $300, you may wipe out one account quickly. That result feels real. You see one less statement, one less due date, and one less source of stress.

3. Likelihood you stick with the plan

Behavior matters. Research in behavioral finance has long shown that people do not always choose the mathematically best path if the path feels hard to maintain. A debt plan fails when you stop using it.

4. Administrative simplicity

Snowball is often easier to follow at a peek. Smallest to largest is simple. Avalanche takes a little more setup because APRs vary and promotional rates expire.

5. Fit for your debt profile

If most of your debt sits on high APR credit cards, avalanche has a stronger edge. If your balances are scattered and one or two are tiny, snowball gives faster wins.

Those five criteria frame the rest of this avalanche vs snowball method review.

Results In Practice: Cost, Motivation, And Speed

This is where avalanche vs snowball method gets practical.

Cost

Avalanche usually wins on cost. That is not opinion. It is math. If two people have the same debts and monthly payment, the one who targets the highest APR first will usually pay less interest over time.

A simple example:

- Debt 1, $2,000 at 28% APR

- Debt 2, $2,000 at 8% APR

- Extra payoff budget, $300 a month after minimums

If you attack the 28% debt first, less interest piles up while you work. If you attack the 8% debt first because it is smaller or tied in size, the 28% balance keeps burning cash.

Over many months, that gap grows.

Motivation

Snowball often wins on motivation. And motivation is not fluff. It affects completion.

If you clear two small debts in the first six months, your plan feels alive. You get proof that your effort changes your numbers. Many people need that feedback loop.

By contrast, avalanche may ask you to stare at one ugly high APR balance for a long time. If that balance is also large, progress feels slow even when you are doing the smart thing.

Speed

The answer depends on what you mean by speed.

- Fastest first payoff, snowball often wins

- Fastest path to lower interest drag, avalanche wins

- Fastest path to total payoff, avalanche often wins if you stay consistent

That last phrase matters. If snowball keeps you engaged and avalanche makes you quit, snowball becomes faster for you in real life.

So in avalanche vs snowball method, cost favors avalanche. Motivation favors snowball. Overall speed depends on whether you keep going month after month.

Pros And Cons Of Each Method

A side by side list makes the avalanche vs snowball method choice easier.

Avalanche method pros

- Saves the most money in many cases

- Reduces high interest debt sooner

- Often shortens total payoff time

- Best match for people who care about efficiency and numbers

Avalanche method cons

- First win may take longer

- Progress may feel slow at the start

- Requires accurate APR tracking

- Harder to stick with if you need visible momentum

Snowball method pros

- Gives quick wins

- Builds confidence early

- Simplifies your debt list faster

- Often easier to keep following during stressful months

Snowball method cons

- Usually costs more in total interest

- High APR debt may stay around longer

- Total payoff time may stretch if expensive balances wait

- The emotional lift comes with a financial tradeoff

Here is a compact comparison.

| Factor | Avalanche | Snowball |

|---|---|---|

| Interest savings | Better | Worse |

| Early momentum | Worse | Better |

| Ease of setup | Moderate | Easy |

| Best for high APR debt | Better | Worse |

| Best for motivation | Moderate | Better |

One more point. Personal finance author Dave Ramsey popularized the snowball method because behavior drives results. On the other side, many financial planners favor avalanche because lower interest means less waste. Both camps have a point.

That is why avalanche vs snowball method is not a pure math contest. It is a fit test.

Avalanche Vs Snowball Compared To Other Debt Payoff Approaches

Avalanche vs snowball method gets most of the attention, yet they are not your only options.

Debt consolidation

You combine multiple debts into one new loan, often with a lower rate if your credit is strong.

Best when:

- You qualify for a lower APR

- You want one payment instead of several

- You have a clear payoff plan after consolidation

Risk:

- Fees may erase savings

- You may run old cards back up after moving balances

Balance transfer card

You move high APR credit card debt to a card with a 0% intro APR for a set period, often 12 to 21 months.

Best when:

- Your credit is good enough to qualify

- You can pay the debt before the promo period ends

Risk:

- Transfer fees are common

- The standard APR after the intro period may be high

Debt management plan

A nonprofit credit counseling agency works with creditors to lower rates and bundle payments.

Best when:

- You need structure and support

- Credit card debt is your main problem

Risk:

- You may need to close cards

- There may be setup or monthly fees

Debt settlement

You or a company tries to settle debts for less than the full amount owed.

Risk is high here.

- Your credit may take a major hit

- Fees may be steep

- Forgiven debt may be taxable in some cases

- Creditors do not have to agree

Bankruptcy

This is a legal reset for serious cases, not a budgeting trick.

If your debt is impossible relative to income, talk with a qualified bankruptcy attorney, not a social media influencer.

For most people with steady income and manageable unsecured debt, avalanche vs snowball method stays the best starting point because both plans are low cost, clear, and under your control.

Verdict: Which Method Should You Choose?

When you compare avalanche vs snowball method, the best choice is the one you will follow long enough to finish.

Choose the avalanche method if:

- You want to pay the least interest

- You have high APR credit card debt

- You are motivated by efficiency and long term savings

- You track numbers well and do not need quick wins

Choose the snowball method if:

- You need fast progress to stay engaged

- You feel overwhelmed by many small balances

- You want fewer monthly payments early

- You have struggled to stick with strict plans before

If you are torn, use a hybrid.

Start with snowball to clear one or two tiny balances. Then switch to avalanche for the rest. That mix is not cheating. It is practical.

Before you choose, do three things.

- List every debt with balance, APR, and minimum payment

- Set one fixed extra payment amount each month

- Build a small emergency fund so you do not swipe a card at the first surprise expense

Avalanche vs snowball method works best when your budget is stable and your plan is simple. Pick one. Start this month. Then keep going until the last balance is gone.

Frequently Asked Questions about Avalanche vs Snowball Method

What is the main difference between the avalanche and snowball debt payoff methods?

The avalanche method targets debts with the highest interest rates first, saving more money on interest. The snowball method focuses on paying off the smallest balances first to build momentum and motivation through quick wins.

Which method saves more money on interest, avalanche or snowball?

The avalanche method generally saves more money because it reduces high-interest debt first, lowering the total interest paid over time compared to the snowball method.

How do I decide whether to use the avalanche or snowball method?

Choose the avalanche method if you want to minimize interest and are motivated by efficiency. Choose the snowball method if quick progress and visible wins help you stay motivated. Sometimes a hybrid approach starting with snowball then switching to avalanche works best.

Can I still pay off my debts faster using the snowball method?

Yes, the snowball method often provides faster initial payoff of smaller debts, which can boost motivation. However, the total payoff time may be longer if higher-interest debts remain unpaid longer.

What are the basic steps to follow when using either avalanche or snowball method?

Make minimum payments on all debts and allocate any extra money toward either your highest interest debt (avalanche) or smallest balance debt (snowball). Once a debt is paid off, roll that payment into the next target debt until all debts are cleared.

Are there other debt payoff strategies besides avalanche and snowball?

Yes, other approaches include debt consolidation, balance transfer cards, debt management plans, debt settlement, and bankruptcy. Each has its benefits and risks, so avalanche or snowball methods often remain the best starting point for most people.

{kind=link}