Emergency fund: how much should you save? The short answer is enough to cover your core bills for at least 3 to 6 months. Your real number depends on your job, health, income, housing costs, and how stable your life feels right now.

A lot of advice stops at a neat rule. Save three months. Save six months. Move on. But your emergency fund should fit your life, not a generic chart.

If your income changes month to month, you need more cushion. If you have a stable job, low fixed bills, and family support, you may need less. The goal is simple. You want cash ready for a job loss, medical bill, car repair, pet emergency, or urgent trip.

This guide breaks down how much emergency savings you need, what expenses to count, where to keep the money, and how to build your fund without stalling the rest of your financial plan.

Why An Emergency Fund Still Matters More Than Ever

An emergency fund matters because life still gets expensive fast. Rent rises. Insurance premiums climb. Cars break down at the worst time. Then one missed paycheck turns into a credit card balance.

That is the main reason emergency savings still sits near the top of any smart money plan. It gives you time. Time to deal with a layoff, or to handle a surprise bill. Time to make a good decision instead of a rushed one.

Recent data keeps pointing in the same direction. Many households still struggle to cover an unexpected expense without debt. Even when inflation cools, the price level stays high. Groceries, utilities, child care, and health costs do not snap back to old numbers.

An emergency fund also protects more than your bank account.

It helps you avoid:

- High interest credit card debt

- Early retirement withdrawals and tax penalties

- Late fees on rent, loans, or utilities

- Selling investments at a bad time

- Taking the first job offer out of panic

There is also a mental side to this. When you know cash is there, everyday money stress drops. You stop treating every surprise like a crisis.

And if you are asking, “Emergency fund: how much is enough?” start here. Enough means you can absorb a real setback without borrowing. Not forever. Long enough to regain control.

That is why the question is not whether you need one. You do. The better question is how large your emergency fund should be for your risks.

How Much To Save Based On Your Income, Bills, And Risk Level

The best way to size your emergency fund is to use your monthly bare minimum expenses, then adjust for your risk level.

Start with the bills you must pay to keep life running:

- Housing, rent or mortgage

- Utilities

- Groceries

- Insurance premiums

- Minimum debt payments

- Gas or transit

- Child care needed to work

- Essential medical costs

- Phone and internet for work and daily life

Now total those numbers. That gives you your baseline monthly survival cost.

Here is a simple example:

- Rent: $1,600

- Utilities: $250

- Groceries: $500

- Insurance: $300

- Minimum debt payments: $250

- Gas and transit: $200

- Phone and internet: $140

- Medical and prescriptions: $160

Total: $3,400 a month

If your target is 3 months, you need $10,200. If your target is 6 months, you need $20,400.

Next, adjust based on your income and risk.

You may need a larger emergency fund if:

- You are self employed

- Your income swings month to month

- You work in sales, freelance, contract, or commission roles

- You support children or other family members

- You own an older car or home with repair risk

- You have health issues or high deductibles

- You are the only earner in your household

You may be fine with a smaller starting target if:

- Your job is stable

- You have two dependable incomes at home

- Your fixed bills are low

- You have no dependents

- You have strong family support in a real emergency

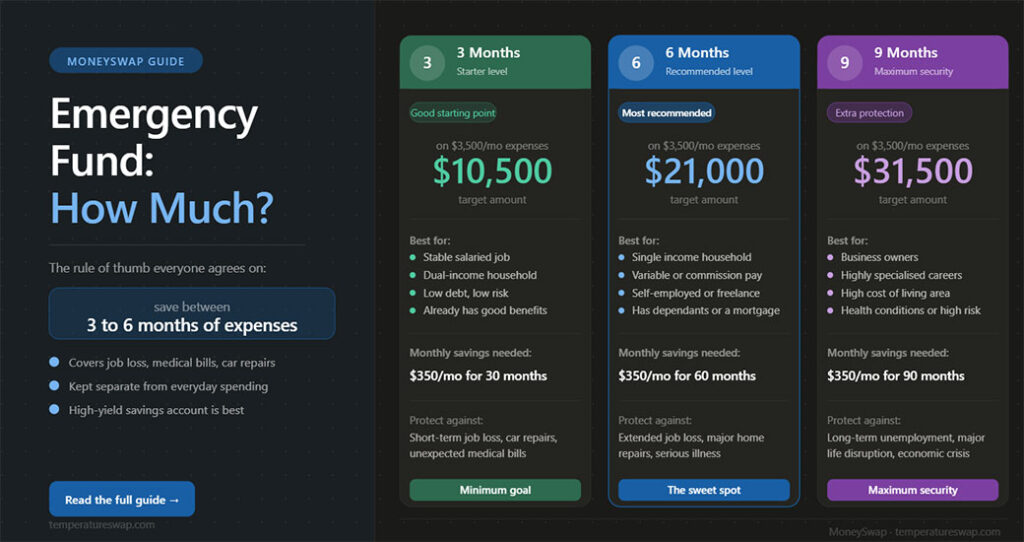

A good rule is this. Stable situation, aim for 3 months first. Medium risk, aim for 4 to 5 months. Higher risk, aim for 6 months or more.

So, emergency fund, how much should yours be? Start with your monthly essentials, then match the number to your real life risk.

The 3-Month Vs. 6-Month Rule And When To Go Higher

The 3 month versus 6 month rule is useful because it gives you a range. Still, you should not treat it like a law.

Three months works well for people with steady pay, low expenses, and a low chance of sudden unemployment. If your job is stable and your household has backup income, 3 months of emergency savings is a solid base.

Six months makes more sense if replacing your income would take time. That includes people in specialized fields, single income households, freelancers, and anyone in a shaky industry.

Go higher than 6 months if your risk is above average.

That might fit you if:

- You are self employed and income is uneven

- You own a business

- You have large medical needs

- You live in an area with high housing costs

- You care for kids, aging parents, or both

- Your work depends on seasonal demand

- A recession would hit your field hard

Think of 3 months as a starter finish line, 6 months as a stronger shield. Think above 6 months as extra protection for unstable situations.

There is one more point people miss. Your emergency fund target does not need to appear all at once. Build in stages.

For example:

- Stage 1: $1,000 for immediate shocks

- Stage 2: One month of bare bones expenses

- Stage 3: Three months of essentials

- Stage 4: Six months or more if your risk calls for it

This step by step approach works better for most people than chasing a huge number from day one. Large goals feel abstract. A first milestone feels doable.

If you are still stuck on emergency fund: how much, ask one question. If your income stopped tomorrow, how long would it take you to recover without debt? Your answer points you toward 3 months, 6 months, or higher.

What Expenses Your Emergency Fund Should Actually Cover

Your emergency fund should cover needs, not every part of your current lifestyle.

That distinction matters. When you build your target, you are planning for survival and stability, not normal spending.

Focus on essential expenses such as:

- Rent or mortgage

- Basic utilities

- Groceries and household basics

- Health insurance and medical needs

- Car payment if you need the car for work

- Gas, transit, or other core transport costs

- Minimum debt payments

- Child care tied to work

- Phone and internet

- Pet essentials if you have pets

Leave out or reduce nonessential spending such as:

- Dining out

- Streaming extras

- Travel

- Shopping

- Gifts

- Hobby spending

- Subscription apps you can pause

This is not about living in misery. It is about knowing what your emergency savings must carry if income drops.

A useful method is to build two budgets.

First, your regular monthly budget. Second, your emergency budget. The emergency version strips spending down to what keeps you housed, fed, insured, employed, and reachable.

For some people, that emergency budget is much lower than their normal spending. That is good news. It means your emergency fund target may be smaller than you thought.

Also, define what counts as a true emergency. Good examples include:

- Job loss

- Major car repair

- Urgent home repair

- Medical bill

- Emergency travel for family

- Vet bill for a serious issue

Poor uses include:

- Holiday shopping

- Concert tickets

- A routine sale you do not want to miss

- Upgrades you did not plan for

Your emergency fund works best when the rules are clear before stress hits. That way you do not raid it for things that feel urgent in the moment but are not.

Where To Keep Your Emergency Savings For Safety And Access

Your emergency savings should stay in a place that is safe, liquid, and separate from your daily spending.

For most people, the best home is a high yield savings account at an FDIC insured bank or an NCUA insured credit union. You want your money easy to reach, while still earning some interest.

A good emergency fund account should offer:

- Fast transfers

- No market risk

- No monthly fees

- No minimum balance traps

- Federal deposit insurance within limits

Why not keep it in checking? Because checking is too easy to drain. One rough month and your emergency money blends into bill money.

Why not invest it in stocks? Because emergencies do not wait for the market to recover. If your balance drops 20 percent right when you need it, that defeats the purpose.

Money market accounts also work for some people. So do cash management accounts with strong protections and quick access. The key is the same. Safety first. Return second.

You can organize the money in one account or split it:

- Tier 1: A small amount in checking for immediate same day needs

- Tier 2: The bulk in high yield savings

- Tier 3: For larger funds, a second savings bucket for job loss only

That setup helps if you tend to dip into savings too often.

One note on access. Easy access does not mean instant spending. You want fast transfer access, not a debit card tied to the account if impulse spending is a problem.

When people ask emergency fund, how much should stay in cash, the answer is simple. All of it. This money is insurance for your life. The job is stability, not growth.

How To Build Your Fund Faster Without Derailing Other Goals

Building an emergency fund takes time, especially when bills already feel tight. So make the process automatic and small enough to stick.

Start with a target you can hit in the next 30 to 60 days. That first win matters. Then raise the bar.

Use these steps:

- Set a starter goal, such as $500 or $1,000

- Open a separate savings account

- Automate transfers on payday

- Send windfalls to savings, tax refunds, bonuses, cash gifts

- Cut one or two expenses and redirect the money

- Sell items you do not use

- Add temporary income if needed

Here is a simple example. If you save $50 a week, you reach about $2,600 in a year. Save $100 a week, and that becomes $5,200. Progress looks slow month to month. Over a year, it adds up.

Try a few practical moves:

- Pause one subscription bundle

- Lower takeout by two meals a week

- Put side gig income into savings only

- Round up transfers after each paycheck

- Bank raises instead of expanding spending

At the same time, avoid building your emergency fund by ignoring high interest debt forever. If your credit card rate is extreme, a split plan often works best. Put some money toward debt and some toward savings until you reach a basic cushion. After that, attack the debt harder.

If your employer offers direct deposit splitting, send part of your paycheck straight into emergency savings. That removes temptation.

And do not wait for the perfect month. The best emergency fund starts small. Then it grows because you keep going, even when progress feels boring.

Conclusion

Emergency fund: how much you need depends on your monthly essentials and your risk. For many people, 3 months is a strong starting point. For others, 6 months or more makes better sense.

Count the expenses that keep your life running. Save the money in a safe, easy access account. Build the fund in stages so the goal feels manageable.

The right number is not random. It is personal. Once you calculate your emergency budget, you will know what your emergency fund should be, and you will have a clear target to work toward.

Emergency Fund: Frequently Asked Questions

How much should I save in an emergency fund?

Typically, you should save enough to cover your essential living expenses for 3 to 6 months. The exact amount depends on factors like job stability, income variability, health, and family obligations.

What expenses should an emergency fund cover?

Your emergency fund should cover essential expenses such as rent or mortgage, utilities, groceries, insurance premiums, minimum debt payments, transportation, child care necessary for work, and essential medical costs.

Where is the safest place to keep my emergency fund?

Keep your emergency fund in a safe, liquid account like a high-yield savings account at an FDIC or NCUA insured bank or credit union, ensuring easy access without market risk or fees.

When should I aim for a 6-month emergency fund instead of 3 months?

Aim for 6 months or more if you have variable income, work in unstable industries, are self-employed, have high medical expenses, or support dependents, as it provides a stronger financial cushion.

How can I build my emergency fund faster without compromising other financial goals?

Start with a small, achievable goal like $500 to $1,000, automate savings transfers, cut discretionary spending, use windfalls like bonuses for savings, and consider side income to accelerate growth.

{kind=link}