Most people, just like me and you, don’t have a spending problem as much as they have a visibility problem. Money comes in, bills get paid, a few card swipes happen here and there, maybe a subscription renews that you forgot about, and by the end of the month you’re left wondering: Where did it all go? That question is exactly why zero-based budgeting has become such a popular method for both individuals and businesses.

What Zero-Based Budgeting Means

At its core, zero-based budgeting is simple: you give every dollar a purpose before you spend it. That purpose might be rent, groceries, gas, savings, your emergency fund, investments, or extra debt payoff.

The goal is not to spend everything just because the word “zero” is in the name. It’s to make sure your income minus your planned expenses equals zero:

Income – Expenses = 0

That “zero” means no dollar is left wandering around without a job. It does not mean your bank account has to hit zero. And it definitely does not mean you can’t save money. In fact, one of the biggest reasons people love a zero-based budget is that it makes saving, debt repayment, and future planning far more intentional.

Why It Works

If you’ve ever tried to budget by simply “being better this month,” you already know how slippery that can feel. Good intentions are nice. A real plan works better.

Zero-based budgeting helps you decide, in advance, how much goes toward essentials, how much goes toward financial goals, and how much you can spend on the fun stuff without guilt. That structure can help you save money more consistently, pay off debt faster, avoid overspending, and make real progress toward goals that usually stay stuck in the someday category.

Why It Feels More Realistic

It also works well because it reflects real life better than vague budget percentages alone. Maybe this month you need to beef up your car repair fund; next month your priority is catching up on a credit card. Maybe you’re preparing for holiday spending, back-to-school costs, or an upcoming move.

A zero-based budget gives you a way to adapt your monthly budget on purpose instead of reacting after the fact.

The Downsides to Know

That said, this isn’t a magic trick. It takes attention. It asks you to look honestly at your spending. And it can feel a little restrictive at first if you’re used to spending first and sorting it out later.

For people with irregular income, like freelancers, gig workers, or commission-based earners, it can also be more complicated because your monthly income may not be predictable enough to assign every dollar neatly at the start of the month. So while zero-based budgeting can be incredibly effective, it isn’t automatically the best budgeting method for everyone.

What This Guide Will Cover

That’s why this guide is practical rather than preachy. You’ll learn what zero-based budgeting is, how zero-based budgeting works, how to build one step by step, and how to avoid the mistakes that make beginners quit too soon.

You’ll also see a beginner-friendly zero-based budgeting example, a more realistic before-vs-after scenario, and side-by-side comparisons with traditional budgeting, the 50/30/20 method, envelope budgeting, and pay-yourself-first.

Tools That Can Help

We’ll also look at tools that make this easier in real life, including budgeting apps, spreadsheets, and manual methods. Each option has tradeoffs.

Some people love the automation and category alerts of budgeting apps. Others trust a spreadsheet because it’s flexible and free. And some people stick best with pen and paper because they need something tangible.

Why It’s Worth Learning

If your main goals are to understand where your money goes each month, stop overspending, save more consistently, or get serious about debt payoff, zero-based budgeting is worth understanding.

Even if you don’t use it forever, learning this method changes the way you think about money. You stop seeing budgeting as a punishment and start seeing it as a way to direct your money toward the life you actually want.

Let’s break it down in a way that feels clear, realistic, and usable.

What Is Zero‑Based Budgeting?

Zero-based budgeting is a budgeting method where you assign every dollar of your income to a exact job until your budget balances to zero.

The core formula is:

Income – Expenses = 0

That sounds more dramatic than it is. You’re not trying to empty your bank account. You’re creating a plan so every dollar has a purpose.

Those purposes can include:

- Fixed bills like rent or mortgage

- Variable spending like groceries and gas

- Savings contributions

- Emergency fund deposits

- Investing

- Sinking funds for future expenses

- Extra debt repayment

- Fun money

That last part matters because a lot of beginners hear “zero-based budgeting” and assume it means they must spend every dollar. Not true. If you assign $300 to savings, $150 to an emergency fund, and $200 to a car repair sinking fund, those dollars have jobs. They’re not unassigned just because they aren’t being spent at a store.

This method is popular in personal finance because it creates awareness. Instead of checking your account balance and hoping there’s enough left, you decide ahead of time where your money goes. Businesses use zero-based budgeting too, though often in a more formal way. In a company setting, departments may need to justify expenses from the ground up instead of simply repeating last year’s budget. The shared idea is intentionality: every dollar should earn its place.

For households, that intentionality can be a game changer. It helps answer questions like:

- Can I actually afford to eat out this week?

- Why am I never making progress on debt?

- How do I save money consistently instead of randomly?

- Why do “small” purchases keep wrecking my monthly budget?

A zero-based budget makes those answers visible.

Example Monthly Budget Table

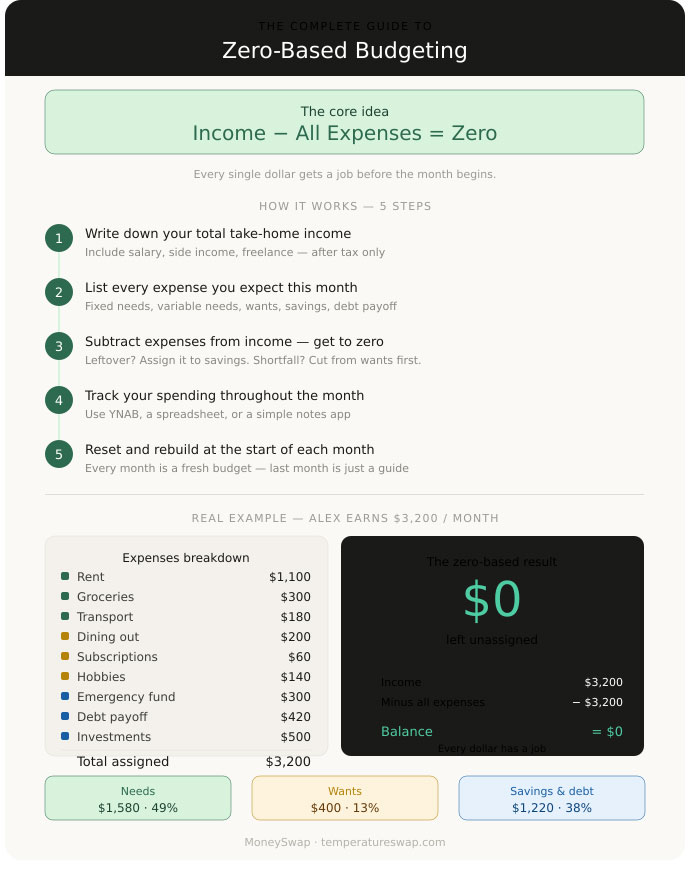

Here’s a simple beginner-friendly zero-based budgeting example for a monthly take-home income of $4,000.

| Category | Planned Amount |

|---|---|

| Rent | $1,200 |

| Utilities | $200 |

| Groceries | $450 |

| Transportation | $250 |

| Insurance | $200 |

| Phone/Internet | $120 |

| Minimum Debt Payments | $300 |

| Extra Debt Payoff | $250 |

| Emergency Fund | $200 |

| Retirement/Investments | $250 |

| Sinking Funds | $200 |

| Dining Out | $150 |

| Entertainment | $80 |

| Personal/Household | $100 |

| Miscellaneous Buffer | $50 |

| Total Assigned | $4,000 |

Using the formula:

$4,000 income – $4,000 assigned = $0 left unassigned

That’s a zero-based budget.

Notice what’s happening here: some money is being spent now, some is going toward future expenses, and some is building long-term security. All of it has a job. That’s the point.

How Zero‑Based Budgeting Works (Step‑by‑Step)

If you’re new to budgeting for beginners, the easiest way to think about this method is: plan first, spend second, adjust as needed. You don’t need perfect numbers on day one. You just need a clear process.

Step 1, Calculate Your Monthly Income

Start with the money you can actually use this month.

For salaried employees, that usually means your monthly take-home pay after taxes, insurance, and deductions while, hourly workers, use a realistic estimate based on your average paycheck. For freelancers or gig workers, use a more conservative number, ideally based on your lowest reliable month rather than your best one.

If your income is irregular, zero-based budgeting gets trickier because you can’t always assign exact amounts confidently at the start of the month. A safer approach is to budget from income already received or to use a baseline income number and prioritize essentials first.

Include:

- Paychecks

- Side hustle income

- Child support or alimony, if dependable

- Other regular income sources

Avoid counting unpredictable windfalls before they happen.

One beginner mistake is budgeting with gross income or with money you hope to earn. That creates a budget that looks good on paper but falls apart in real life.

Step 2, List and Categorize All Monthly Expenses

Next, write down everything your money needs to do.

A good starting point is to group expenses into categories such as:

- Housing

- Utilities

- Food

- Transportation

- Insurance

- Debt payments

- Savings

- Investments

- Sinking funds

- Personal spending

- Entertainment

- Miscellaneous

Then split them into three buckets:

- Fixed essentials: rent, insurance, loan minimums

- Variable essentials: groceries, gas, utilities

- Goals and flexible spending: savings, extra debt payments, dining out, hobbies

This step is where many people discover why they feel broke even though decent income. It’s often not one giant expense. It’s the accumulation of frictionless spending, ignored annual bills, and categories that were never planned at all.

Step 3, Assign Every Dollar a Job

Now allocate your income across those categories until you reach zero.

Start with the must-pay items first:

- Housing

- Utilities

- Food

- Transportation

- Insurance

- Minimum debt payments

Then assign money to priorities like:

- Emergency fund

- Retirement contributions

- Sinking funds

- Extra debt payoff

Finally, assign amounts for discretionary spending too. Yes, really. A zero-based budget that leaves out fun money tends to fail because it’s too rigid to last.

If the numbers don’t work, don’t panic. That’s not failure: that’s information. Reduce lower-priority categories until your budget balances.

Step 4, Track, Adjust, and Repeat Every Month

A zero-based budget is not “set it and forget it.” It’s a living plan.

During the month, track what you spend and compare it with what you planned. If you overspend on groceries by $40, you’ll need to move $40 from another category. That is still zero-based budgeting. The goal is not perfection. The goal is awareness and intentional adjustment.

At the end of the month, review:

- Which categories were realistic?

- Which ones were too low?

- Did any annual or irregular expenses sneak up on you?

- Did your spending match your values?

Then build next month’s budget with better numbers.

That repeating cycle is what makes zero-based budgeting effective. It teaches you your real spending patterns, not the fantasy version. Over time, your monthly budget gets less stressful and far more accurate.

Why Zero‑Based Budgeting Works

Zero-based budgeting works because it removes vagueness. A lot of money stress comes from not making decisions until the money is already gone.

Gain Control and Cut Waste

When every dollar has a role, random spending becomes easier to spot. You start noticing the subscriptions you forgot about, the casual takeout habit that costs more than you realized, or the “just this once” purchases that happen every week.

That doesn’t mean every extra purchase is bad. It means you can finally see the tradeoffs.

This is why zero-based budgeting often feels powerful so quickly. Within one or two months, many people stop asking where their money went because they already know.

Make Saving Intentional and Pay Off Debt Faster

Saving money gets easier when it becomes a budget category instead of an afterthought. Same with debt reduction.

Without a plan, savings often become whatever happens to be left over at the end of the month. Usually, that’s not much. In a zero-based budget, you assign money to your emergency fund, sinking funds, investments, or extra debt payments before lifestyle spending expands to consume it.

That doesn’t guarantee fast results overnight, but it creates consistency. And consistency is what helps you pay off debt faster over time.

Clarify and Achieve Financial Goals

A vague goal like “I should save more” doesn’t compete well against daily spending. A defined allocation does.

Zero-based budgeting connects your monthly decisions to bigger goals:

- Building a starter emergency fund

- Paying off a credit card

- Saving for a car

- Preparing for holiday spending

- Investing for retirement

That clarity matters. It turns money into a tool instead of a source of constant low-level anxiety.

Comparing Zero‑Based Budgeting to Other Methods

No single budgeting style works for everyone. Zero-based budgeting is detailed and hands-on, which can be a strength or a drawback depending on your personality, income stability, and goals.

Zero‑Based vs Traditional Budgeting

Traditional budgeting usually means estimating income and setting broad spending limits by category, often based on prior months. It can be fairly loose. Zero-based budgeting is more exact because every dollar gets assigned before the month unfolds.

| Feature | Zero-Based Budgeting | Traditional Budgeting |

|---|---|---|

| Core idea | Every dollar gets a job | Spend within general category limits |

| Formula | Income – Expenses = 0 | Income – Expenses = surplus/leftover |

| Planning style | Detailed and proactive | Broader and often less exact |

| Savings approach | Planned upfront | Often whatever is left over |

| Best for | People wanting tight control | People wanting simpler oversight |

| Downside | More time and tracking | Easier to drift or overspend |

If you often wonder where your money went, zero-based budgeting usually gives better visibility. If you already spend fairly predictably and just need loose guardrails, traditional budgeting may feel easier.

Zero‑Based vs 50/30/20, Envelope, and Pay‑Yourself‑First

Here’s how zero-based budgeting compares to other common budgeting methods.

| Method | How it works | Strengths | Weaknesses | Best fit |

|---|---|---|---|---|

| Zero-based budgeting | Assign every dollar a job | High awareness, flexible priorities, great for debt payoff | Time-intensive, can feel restrictive | Detail-oriented people who want control |

| 50/30/20 | Split income into needs, wants, savings/debt | Simple, fast, beginner-friendly | Too broad for some households: not precise | People who want a lightweight structure |

| Envelope method | Use cash envelopes for spending categories | Strong spending discipline, visual limits | Less convenient in a digital industry | Overspenders who benefit from hard caps |

| Pay-yourself-first | Save first, spend the rest | Great for automating savings | Less visibility into detailed spending | People whose main goal is consistent saving |

The 50/30/20 method is easier to maintain, but it won’t always tell you why you overspent on groceries or subscriptions. The envelope method is excellent for controlling problem categories but can be clunky if most of your spending is digital. Pay-yourself-first is great if your big issue is failing to save, but it may not solve chaotic day-to-day spending.

Zero-based budgeting shines when you want intentional spending and tighter control. It struggles when you want budgeting to be mostly automatic or when your income changes wildly month to month.

The Biggest Advantages of Zero‑Based Budgeting

This budgeting method has a loyal following for a reason. When it fits your personality and life, it can change the way you use money.

Improved Money Management and Intentional Spending

A zero-based budget forces clarity. Instead of reacting to spending after it happens, you make decisions in advance.

That helps with:

- Reducing impulse purchases

- Catching forgotten expenses

- Setting realistic category limits

- Spending on purpose instead of by habit

This is one of the biggest advantages for people who feel like money leaks out in small amounts.

Faster Debt Repayment and Stronger Savings Habits

If your goals are to save money consistently or pay off debt faster, this method is especially useful.

Why? Because it treats financial goals as required jobs for your money, not optional leftovers. You can budget:

- $100 to a starter emergency fund

- $200 to a sinking fund

- $300 extra to credit card debt

- $250 to retirement investing

That kind of structure builds habits. And habits are what move finances forward.

Less Stress and Greater Financial Clarity

Budgeting sometimes gets framed as restrictive, but uncertainty is often more stressful than planning.

Knowing your bills are covered, your savings are growing, and your spending money has a limit can actually reduce anxiety. You stop negotiating with yourself at every purchase because you’ve already made many of those decisions.

It won’t eliminate all money stress, especially if income is tight. But it can reduce the chaos.

Disadvantages, Risks, and Common Mistakes to Avoid

A balanced look matters here. Zero-based budgeting is effective, but it’s not effortless.

Time, Tracking Burden, and Burnout

This method takes more maintenance than simpler budgeting methods. You need to plan, track spending, and adjust categories throughout the month.

For some people, that level of involvement feels empowering. For others, it becomes exhausting.

Common frustrations include:

- Spending too much time categorizing transactions

- Feeling guilty every time a category changes

- Trying to make the budget unrealistically perfect

- Giving up after one messy month

If you’re naturally resistant to detail, this can feel like too much admin for daily life.

Challenges for Irregular Income & Unexpected Expenses

Zero-based budgeting can be harder for freelancers, seasonal workers, commission-based earners, and gig workers because income may change every month.

When you don’t know exactly what you’ll earn, assigning every dollar ahead of time gets tricky. You may need to:

- Budget only income already received

- Use a bare-bones budget first

- Build a larger buffer fund

- Prioritize essentials before flexible spending

Unexpected expenses also expose weak spots fast. If you forget annual subscriptions, car repairs, gifts, medical costs, or school fees, your budget can feel like it failed. Really, the plan just needs better sinking funds.

Top Mistakes to Avoid

Some beginner mistakes show up again and again:

- Confusing assigned dollars with spent dollars

Savings, debt payoff, and sinking funds all count as jobs.

- Forgetting irregular expenses

Annual bills are still real, even if they don’t happen monthly.

- Making categories too strict

A budget with no room for real life usually breaks.

- Not tracking during the month

A budget you never check becomes wishful thinking.

- Quitting after overspending

Overspending in one category doesn’t mean the whole method failed.

- Using unrealistic income estimates

Especially risky with irregular income budgeting.

The fix for most of these is not perfection. It’s consistency, review, and adjustment.

Best Apps, Tools, and Templates for Zero‑Based Budgeting

The best tool is the one you’ll actually keep using. Zero-based budgeting can be done with apps, spreadsheets, or manually. Each has tradeoffs.

Budgeting Apps (YNAB, EveryDollar, PocketGuard, Monarch)

Budgeting apps can make zero-based budgeting easier by automating transaction imports, category tracking, and progress updates.

Pros:

- Faster tracking

- Easier category adjustments

- Mobile access

- Visual reports and alerts

Cons:

- Some require paid subscriptions

- Bank syncing can be imperfect

- You may rely on automation instead of awareness

A few well-known options:

- YNAB: Very aligned with giving every dollar a job: strong for active budgeters.

- EveryDollar: Simple interface, especially approachable for beginners.

- PocketGuard: Helpful for seeing spendable cash after bills and goals.

- Monarch: Broad household finance features and shared visibility for couples.

Spreadsheet Templates (Google Sheets, Excel)

Spreadsheets are a great middle ground between flexibility and control.

Pros:

- Low cost or free

- Fully customizable

- Good for people who like seeing the whole picture

- Easy to tweak categories and formulas

Cons:

- Requires manual updates unless you build integrations

- Easier to abandon if you dislike spreadsheets

- More setup time at the beginning

Google Sheets is great if you want access across devices. Excel is strong if you like deeper customization.

Manual Methods (Notebook, Envelope Adaptations)

Some people simply budget better when the process is physical.

Pros:

- Very low tech and inexpensive

- Helps you slow down and think about spending

- Can feel more tangible and intentional

Cons:

- No automation

- Harder to analyze trends over time

- More effort to update and correct

A notebook works well for people who want a simple monthly budget without app fatigue. Envelope adaptations can also work if you need stronger spending control in categories like groceries, dining out, or personal spending.

Practical Tips for Beginners and Who Should Use It

Zero-based budgeting gets much easier when you stop trying to do it perfectly.

Starter Tips, Keep It Simple and Sustainable

If you’re just starting, try these beginner-friendly tips:

- Start with broad categories, then refine later

- Use last month’s bank statements to estimate spending

- Add a miscellaneous buffer category

- Include fun money so the budget feels livable

- Review your budget weekly, not obsessively daily

- Create sinking funds for non-monthly expenses

- Make savings automatic where possible

The goal is not a beautiful spreadsheet. The goal is a usable system.

Who Should (and Shouldn’t) Use Zero‑Based Budgeting

Best fit:

- People who don’t know where their money goes

- People trying to pay off debt faster

- Savers who need more structure

- Couples who want a shared spending plan

- Anyone who likes hands-on control

Poor fit or harder fit:

- People who strongly dislike tracking details

- Households with highly irregular income and no buffer

- People who want a very simple rule-of-thumb budget

- Anyone who becomes overly anxious from micromanaging categories

You can also use a hybrid approach. For example, run a zero-based budget for core bills, savings, and debt goals while keeping discretionary categories broader. That often feels more realistic than trying to control every tiny expense.

Real‑Life Example and Before‑vs‑After Walkthrough

Theory helps. Seeing how this plays out in real life helps more.

Before vs After Scenario

Before:

Jordan earns $4,200 a month. Bills get paid, but the rest feels fuzzy. Some months Jordan saves $50. Other months, nothing. Credit card debt stays stuck around $5,000. Dining out, convenience spending, and random online purchases quietly eat up the margin.

After using zero-based budgeting:

Jordan assigns every dollar:

- Bills and essentials covered first

- $400 extra toward credit card debt

- $200 to emergency savings

- $150 to a car repair sinking fund

- $120 for dining out

- $75 for personal spending

After three months, Jordan knows where the money goes, has fewer surprise shortfalls, and is making measurable progress. The debt isn’t gone overnight, but the direction is finally clear.

Sample Monthly Walkthrough

Let’s say your monthly take-home income is $3,500.

You assign:

- Rent: $1,100

- Utilities: $180

- Groceries: $400

- Gas/Transportation: $220

- Insurance: $170

- Phone/Internet: $110

- Minimum debt payments: $250

- Extra debt payoff: $200

- Emergency fund: $150

- Sinking funds: $150

- Retirement/investing: $150

- Dining out: $100

- Entertainment: $70

- Personal care/household: $100

- Buffer: $150

Total assigned = $3,500

Mid-month, groceries run $35 over. You move $20 from entertainment and $15 from buffer. That’s normal. Zero-based budgeting is not broken because you adjusted it. The adjustment is part of how zero-based budgeting works.

That flexibility is what makes it usable in real life instead of just in theory.

Frequently Asked Questions (FAQ)

What is the main goal of zero‑based budgeting?

The main goal is to give every dollar a purpose so you have more control over spending, saving, and financial goals. It helps reduce waste and increase intentional spending.

Does zero‑based budgeting mean spending all your money?

No. It means assigning all your money. Dollars assigned to savings, emergency funds, investments, or debt repayment still have jobs even if they aren’t immediately spent.

Is zero‑based budgeting good for beginners?

Yes, especially for beginners who want a clear view of where their money goes. It can feel detailed at first, but it’s very teachable because the formula is simple and the structure is practical.

How often should you update your budget?

At minimum, review it weekly and adjust when spending changes. Most people create a fresh zero-based budget each month because bills, goals, and variable expenses change.

Can zero‑based budgeting help save money?

Yes. It makes saving money a planned category rather than a leftover amount. That often leads to more consistent progress.

What happens if you overspend in one category?

You move money from another category and rebalance the budget. The goal is not perfection. It’s staying aware and making intentional tradeoffs.

Is zero‑based budgeting good for irregular income?

It can work, but it’s harder. If your income varies, budget based on money already received or on a conservative baseline, prioritize essentials first, and build a larger buffer. For some people with highly unpredictable income, a looser budgeting method may feel easier to sustain.

Zero-based budgeting is powerful because it makes your money decisions visible. Every dollar gets a purpose. That’s the whole idea, and it’s what makes this method so effective for saving money, reducing overspending, and making faster progress on your goals.

If you’re curious whether it will work for you, try it for one month. Not forever. Just one real month with your real numbers. You’ll learn quickly where your money is going, what matters most, and what needs adjusting.

The sooner you control your money, the sooner your money stops controlling you.

Frequently Asked Questions about Zero-Based Budgeting

What is the main goal of zero-based budgeting?

The main goal of zero-based budgeting is to assign every dollar a specific job before you spend it, ensuring your income minus expenses equals zero, which helps control spending, improve saving, and meet financial goals intentionally.

How does zero-based budgeting help with saving money?

Zero-based budgeting makes saving a planned category rather than an afterthought by assigning money upfront to savings, emergency funds, or investments, leading to more consistent progress and faster debt repayment over time.

Is zero-based budgeting suitable for people with irregular income?

Zero-based budgeting can work for irregular income earners by budgeting only with money already received, prioritizing essentials, and building a larger buffer, though it can be more complicated and may require adapting the method for stability.

How often should I update my zero-based budget?

You should at least review your zero-based budget weekly and adjust as needed during the month since spending and priorities can change. Many people create a fresh budget each month to reflect updated bills and goals.

What is the difference between zero-based budgeting and traditional budgeting?

Zero-based budgeting assigns every dollar a role before the month starts, balancing income and expenses to zero, while traditional budgeting sets broader category limits based on past months, often leaving income minus expenses with a leftover amount or surplus.

Can zero-based budgeting reduce overspending and financial stress?

Yes, because it increases spending awareness by assigning every dollar a purpose, making unexpected purchases visible, and reducing vagueness, which helps cut waste and lowers stress by clarifying where your money goes each month.

{kind=link}